Darren Hughes, director of CASHOFF Europe, told ShareSpot about the future of OpenAPI, the development of banking apps and the solutions offered by CASHOFF.

Business strategy during the 2020 pandemic

COVID-19 has seriously affected the entire global economy. Many industries and companies are having difficult times. And for many companies it’s a good time to take stock and identify next moves.

For CASHOFF that means to actively research new markets, competitors, and existing solutions in those regions. This gives us a deeper understanding of the environment before entering new regions.

The result of such research should be a complete analysis of the available functionality of data solutions for each large financial service company. Then we can simply identify how we can help the bank bring it to a next level. To get higher engagement, more cross sales or better lending decisions.

During the pandemic, equal attention must be paid to both current and potential customers.

Everything must works clearly and without interruptions so that all parties are satisfied with the partnership. So whilst its import to look for new customers don’t forget the existing ones.

It is also important for potential clients to speak to them in the same language, or at least understand the position they are in, how covid is effecting them and explain how other clients are coming through this period. .

Good research should give a complete understanding of what they are doing and what they need.

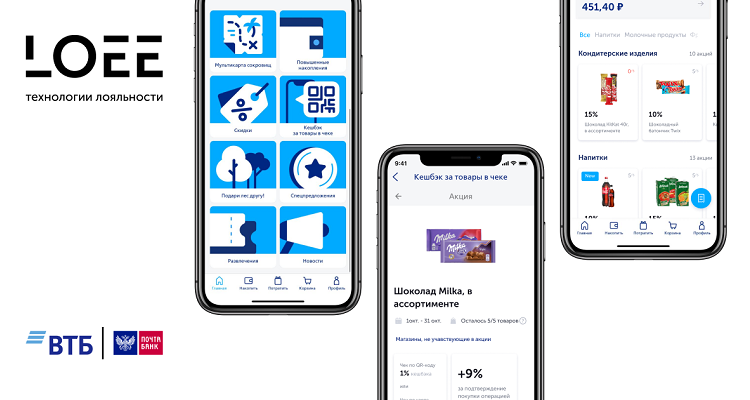

Brand-funded cashback

CASHOFF’s unique cashback solution is brand funded and not linked to a particular store. Here CASHOFF is targeting grocery stores and supermarkets. People shop there on a daily basis, which creates a high volume of transactions, in contrast to, for example, the purchase of shoes.

This approach means banks can lower their loyalty costs straight away, see more engagement in their app – whilst potentially increasing revenue too.

OPEN API provide for tailor-made solutions

CASHOFF also offers a tool to increase customer loyalty and engagement.

Open API in Europe made it possible to aggregate in one app the data of accounts, expenses, loyalty programs, e-wallets and loans.

Thus users can monitor their finances in a comfortable way. And for the bank, whose app displays such data, this allows a deeper analysis of users.

As a result, knowledge of the customer’s savings or loans enables the bank to make more relevant offer to the client. And to make those decisions quickly.

Personalized relationships with users are a key trend for the foreseeable future. Therefore, it is important to start building them right now. Today, even in the UK, tailor-made offers are still not at a high standard. As an example, Darren said that his bank’s app shows him the same loan offer for 2 years and no other promotion. That seems like a missed opportunity.

Personalization is mutually beneficial for both parties.

The research in Europe found that 74% of customers are willing to provide more personal data to trusted companies in exchange for discounts on products that are in demand. This information, using Data Science and ML, allows to predict user behavior. Thanks to this it will be possible to offer to customers not only certain familiar products, but also something relating to them.

OpenAPI is gradually being developed and implemented in many countries. Fintech startups with secure access to banking data can propose and implement solutions much faster than internal banking resources. Outdated software of banks, unable to adapt in time, will lead them to collapse.

Current trend: banks compete with finch startups

Competition among banks and fintech startups is growing. At the same time profit margins of traditional banking services are constantly decreasing. Because of this, in the next 2-3 years, banks will strive to receive income from additional functionality in their apps. And accordingly the number of new services will grow. The survival of absolutely all banks in the new realities depends on this.

In turn, fintech startups should take into account the differences between each bank and create a flexible product that will be easy to modify for different needs and target audiences. Banking services for the business segment are also changing.

Many market players have not had significant innovations for more than 10-15 years. Therefore, the trends for b2b will be similar to b2c products like data analytics, aggregation of data from different sources in one place, detailed analytics of income and expenses.

Final advice

Darren concluded with the advice: Never rely on just one marketing channel.

In the past, Darren has seen the consequences of this mistake first hand. When the main channel got into trouble, they lost 90% of new leads overnight. It is very important to diversify channels, although some of them may cost more.

For example, a significant proportion of companies that rely solely on exhibitions have completely lost sales during the pandemic.